|

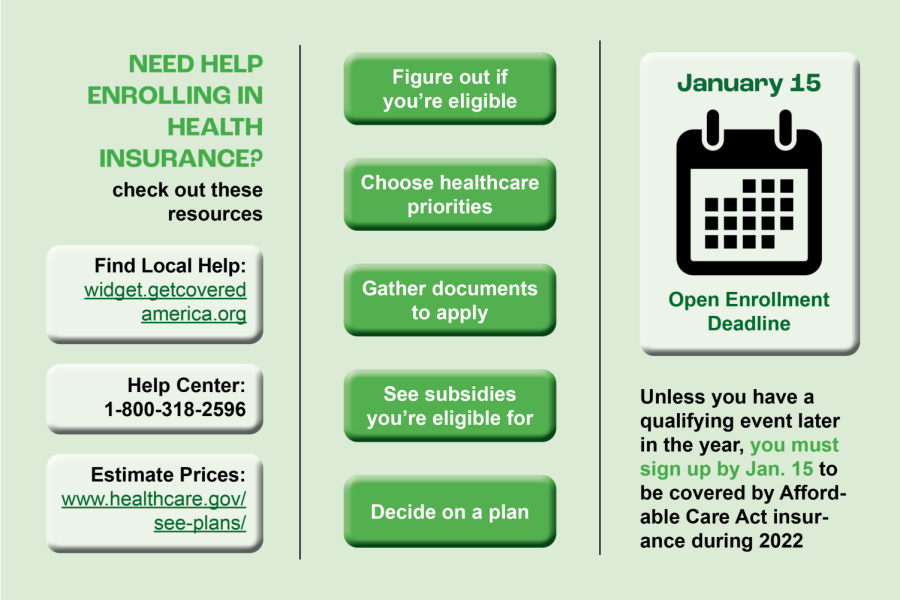

: The terms 'covered advantage' and 'covered' are utilized regularly in the insurance coverage industry, however can be confusing. A 'covered advantage' generally refers to a health service that is consisted of (i. e., 'covered') under the premium for a provided medical insurance policy that is paid by, or on behalf of, the registered client. 'Covered' indicates that some portion of the permitted cost of a health service will be thought about for payment by the insurer. It does not imply that the service will be paid at 100%. For example, in a strategy under which 'urgent care' is 'covered', a copay may apply. If the copay is $100, the patient needs to pay this quantity (generally at the time of service) and then the insurance coverage plan 'covers' the remainder of the enabled expense for the immediate care service. In some circumstances, an insurance provider may not pay anything towards a 'covered benefit'. For instance, if a patient has not yet met an annual deductible of $1,000, and the expense of the covered health service supplied is $400, the client will need to pay the $400 (often at the time of service). What makes this service 'covered' is that the cost counts toward the yearly deductible, so only $600 would stay to be paid by the patient for future services prior to the insurer starts to pay its share. If you have concerns about how the health reform law will impact you and your insurance coverage alternatives, please go to Health care. gov, or call their Assistance Center at 1-800-318-2596 if you have questions that can not be responded to on their site. You can also call your state's Customer Help Program, Exchange, or Medicaid office with questions about eligibility and enrollment. KFF has the ability to supply individual recommendations on your insurance coverage options. However, we do supply responses to a variety of often asked questions below, along with more in-depth questions and answers in our Health Reform Frequently Asked Question page. It might be that you are utilizing an older variation of Internet Explorer or Firefox.

Uncertain which browser variation you are running? Examine here for IE or here for Firefox. If you continue to have technical issues with the Calculator after updating your web browser, please contact KFF. Please note that we have the ability to offer specific advice or assistance understanding your results. If can you sell your timeshare you have additional concerns, we recommend that you contact Health care. gov timeshare foreclosure laws or your state's Medical insurance Market to learn more. Yes, the calculator now shows premiums for 2021 in all states. No. The calculator is planned to show you an estimate of just how much you might pay and the quantity of financial aid you may be eligible for if you purchase coverage through the Medical insurance Market.

gov, your state's Medical insurance Market, or Medicaid program workplace. Although the Health Insurance Coverage Market Calculator is based on actual premiums for strategies sold in your area, there are a number of reasons that your calculator results might not match your actual tax credit quantity. For instance, the calculator relies completely on information as you enter it, whereas the Marketplace may compute your Modified Adjusted Gross Earnings (MAGI) to be a different amount or might confirm your income against previous year's data. Has the calculator been updated for the changes enacted through the American Rescue Plan Act (ARP) of 2021 (COVID-19 relief)? Yes, the calculator approximates how much you might pay and the quantity of monetary help you will get under the American Rescue Plan Act (ARP), the COVID-19 relief law passed in March 2021. If you're getting unemployment payment throughout 2021, see Frequently Asked Question listed below. Aids are monetary support from the Federal government to help you pay for health coverage or care. The amount of help you get is determined by your income and household size. There are two kinds of health insurance coverage subsidies readily available through the Marketplace: the and the. helps decrease your regular monthly premium expenses. This subsidy is available to people with household incomes above 100% of the poverty line who purchase protection through the Health Insurance Market. These people and households will have to pay no greater than 0% - 8. How Much Is Cobra Insurance - The Facts

Anything above that is paid by the government. The amount of your tax credit is based upon the cost of a silver strategy in your area, however you can use your premium tax credit to purchase any Marketplace plan, including Bronze, Gold, and Platinum plans (these different kinds of plans are explained below). You can select to have your tax credit paid straight to the insurance provider so that you pay less every month, or, you can decide to wait to get the tax credit in a lump sum when you do your taxes next year. KFF FAQs provide additional details about how premium tax credits work. These subsidies are only readily available to individuals buying their own insurance who make in between 100% and 250% of the poverty level (improved cost sharing subsidies are available for Native Americans at somewhat higher earnings levels). If you certify for a cost-sharing aid, you would need to sign up for a silver plan to benefit from it. Unlike the exceptional tax credit (which can be utilized for other "metal levels"), cost-sharing subsidies only deal with silver strategies. With a cost-sharing aid, you still pay the exact same low monthly rate of silver plan, but you also pay less when you go to the physician or have a hospital stay than you otherwise would. If you have more particular concerns about your subsidy, you can consult our Frequently Asked Question pages or call an assister or navigator through Health care. gov or your state's Market. The Health Insurance Marketplace Calculator permits you to go into home income in regards to 2021 dollars or as http://holdenmdje536.jigsy.com/entries/general/rumored-buzz-on-what-is-a-deductible-in-insurance a percent of the Federal poverty line. Home income consists of incomes of the individual who pays taxes, the partner, and, sometimes, children, called dependents on income tax return. How much is life insurance. For the purposes of the calculator, you should enter your best guess of what your income will remain in 2021. When you go to Healthcare. Eligibility for exceptional tax credits is based upon your family's Modified Adjusted Gross Earnings, or MAGI. Your newest tax return will show your Adjusted Gross Income (AGI). For many individuals, MAGI is the exact same or extremely near to adjusted gross earnings. MAGI modifies your Adjusted Gross earnings by including any non-taxable Social Security benefits you may receive, any tax-exempt interest you may earn, and any foreign income you earned that was left out from your income for tax functions. The calculation does not consist of earnings from presents, inheritance, supplemental security earnings (SSI), and some other earnings sources. To learn more, see here - What is pmi insurance.

0 Comments

You can include this rider after buying the policy. Long term care (LTC) rider, Spends for LTC expenses if you fulfill specific requirements. Policy purchase option, Offers you the legal right to purchase additional insurance coverage without proof of insurability. For example, you may wish to increase your life insurance protection after the birth of a child. Waiver of premium rider, Waives premiums if you end up being handicapped or unemployed. (Terms vary by insurance provider.) Just like any kind of life insurance coverage, the death advantage amount you choose at the start of your policy does not have actually an assigned use. With whole life, these funds generally cover funeral expenditures, any staying debts and supply a small inheritance. It is necessary to note that the death benefit can be used by recipients in any method they choose. Given that there's no legal requirement for them to spend it on the items that you planned, it's a good idea to choose your recipients carefully. You can also pick multiple beneficiaries, allowing you to split up the cash between member of the family the method you desire. Any requirement for how the cash ought to be invested, such as paying off a home loan or college tuition for children or grandchildren, ought to be specified in a will. For lots of individuals, it's valuable to review why you need life insurance coverage in order to make the determination between term or whole life insurance coverage.State Farm Insurance says that entire life can be an appealing alternative for any of these factors: Others are depending on you for long-term financial support. You want to build up cash worth and secure your beneficiaries. What is comprehensive insurance. You want to produce an estate for your beneficiaries after your death. Your beneficiaries require the benefit to pay estate taxes when you pass away." Whole life does two things for you: safeguards your household and allows you to save for the future," states Scott Berlin, senior vice president and leader of the Group Subscription Association Department at New York Life. Here's how term and entire life vary: Desire a lower premium, Can afford a higher premium, Desired a much shorter dedication, Want no expiration date, Won't have many expenses at theend of the term like a home mortgage, Want cash left to beneficiaries, Don't care about developing money worth, Want to develop cash value, Desired a high amount of coverage, Desired a fairly conservativeinvestment accountFabric, a Brooklyn, NY-based life insurance broker says whole life insurance might be wiser than term life for families with lifelong dependents, families using life insurance coverage as a wealth management tool and households who want to use a life insurance coverage benefit to pay estate taxes. All about How Does Gap Insurance Work

Once your money worth is developed, you can access it for anything retirement, your kid's college tuition or the holiday you've always desired. Whole life policies might be qualified to earn dividends (depending on the company and not ensured). These can be utilized in a range of ways, such as supplying paid-up additional life insurance coverage, which increases both the life insurance benefit and money value." Purchasing term resembles leasing your insurance," says Berlin. "You don't construct up any recurring value. Whole life resembles owning a home you construct up equity." Berlin cautions versus purchasing term life insurance even if it's low-cost life insurance choice." When you're 35, you think that 20 years is a long time, however life does not always work out like you think," he says.

Later on, you might have the ability to convert your term life policy to whole life. For the rich with big estates, putting an entire life policy into a trust can you sell timeshares is a method to prevent paying substantial estate taxes when they die. Here are typical circumstances that you can review to help identify your protection need. One strategy is to pick a bigger term life policy during higher-debt years (e. g. mortgage, student loans, child expenditures) and likewise acquire a smaller sized entire life policy, expecting far fewer debts as you age (e. g. home loan has actually been settled, children are grown) The next action is to identify your amount of coverage. com has produced a Life Insurance Calculator to assist determine a recommended protection quantity. Here are the major elements that are considered: Funeral costs, Outstanding debt, College-bound children, Income replacement, If you aren't worried about income replacement for a spouse, the policy amount might come with no responsibility to your beneficiaries. If you have no financial obligations to pay and final funeral costs have been arranged, this is a method to leave a tax-free financial present to your beneficiaries. The quantity of the policy will be merely chosen by just how much you would like to bestow. A recipient can be a relative, but it doesn't need to be. Getting My How Much Is Medical Insurance To Work

It's not uncommon for individuals to leave their policies to charitable organizations or a college almamater. Be sure to plainly time share lawyers name and inform your beneficiary. And if the recipient is an organization, alert the person in charge of charitable planning/donations. https://jaspermukg641.shutterfly.com/173 Keeping the recipient a secret can develop legal issues that might hinder your dreams. If you will not have any financial obligations, and you don't have a need for leaving a present of cash to a beneficiary, a little policy in order to cover your last funeral service costs might be all you require. With simply a little thought and effort, you can pre-plan your funeral service and last costs. If there are any funds left over, they would be provided to your secondary recipient. A whole life policy's rate varies greatly depending on your age, health and habits. Due to the ensured payment, the premiums are considerably more than term coverage. However, do not assume that a policy is out of reach since of cost. Eighty percent of consumers misjudge the expense of term life insurance coverage, according to LIMRA. And the perceived cost prevents over 60% of millennial and Gen Xers from buying any life insurance coverage at all. In order to get a closer concept of what the costs could look like, review the whole life insurance coverage sample premium comparison chart from AAA of Southern California. Nevertheless, the advantage related to such a policy typically passes beyond probate, meaning no will is necessary to ensure your life insurance coverage pay is performed to called recipients. When you buy a life insurance policy, you'll be asked to submit a type that names a recipient. That specific or group of individuals will get the benefit of your policy after you die. No will is needed to ensure the cash gets to the ideal location. Nevertheless, listing your whole life insurance coverage policy in your will can assist enjoyed ones know that the policy exists and can point them in the ideal direction in regards to gathering the advantage. |

RSS Feed

RSS Feed